Invest in Netflix? Make Money with this NFLX Stock Breakdown

Invest in Netflix? Make Money with this NFLX Stock Breakdown

Netflix just reported earnings to kick off earnings season for technology stocks. We’ve got a lot of big names coming up like TSLA 0.00%↑ and AMZN 0.00%↑ which I’ll cover in the coming weeks.

The NFLX 0.00%↑ Q1 report was a mixed bag. The company posted a great quarter, but forecasted a weaker 2nd quarter than expected. I anticipate a lot of ugly Q2 guidance to come from the other companies set to report.

The market was on fire, we had 12 weeks to start the year of stocks going straight up, but as you can see in the chart, the last 3 weekly candles have closed deep in the red.

The market was going up based on a lot of AI hoopla companied with the expectation we were getting 3 interest rate cuts this year. It’s starting to seem like rate cuts may be off the table, we may even see a rate hike since inflation is not going away.

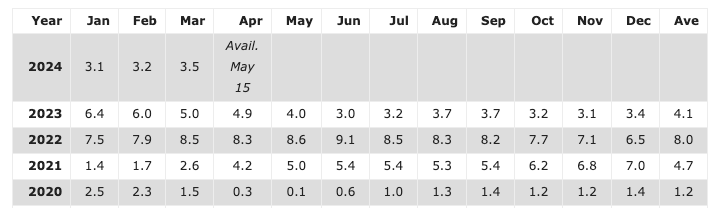

Here is a chart of inflation, which by the way the media likes to mislead you whenever it’s discussed. For example, as you can see in March we only had 3.5% inflation, they will say as some justification that inflation is decreasing. The reality is this is a year over year number. Inflation in March of 2024 was ONLY up 3.5%… over March of 2023 when it was up 5%, over March of 2022 when it was up 8.5% and so on. The reality is if you add up all these numbers all the way back to 2020, for the month of March you get the actual inflation rate in 2024 compared to 2019, which is 21.1%.

Your dollar is worth 21.1% less than it was in 2019, goods are indeed 21.1% more expensive. So inflation may be decelerating but it has not gone down. The picture is even worse when you look at food, as you can probably tell when you go to the grocery store. Basically, everything that is essential costs a lot more: food, energy, insurance and housing.

But, it’s not all bad:

As the saying goes, there’s always a bull market somewhere.

Let’s look at the Netflix report and if the company is worth investing in. Netflix is the clear streaming winner of the traditional players and that is something I’ve been saying for years. Netflix is very similar to Tesla in that regard: the first mover and simply the best in class.

They had a good report, but because their Q2 guide missed estimates companied with the decision that they will stop reporting quarterly subscriber metrics led to the stock dropping nearly 10% on Friday.

Neither of those things matter, but I will touch on 2 things to worry about later. As I said many will have a bad Q2, just look at those inflation numbers above to see why. The decision to stop reporting subscriber metrics is not out of the ordinary, Apple did something similar in 2018 when they stopped reporting unit sales.

Netflix said it’s because it won’t paint an accurate picture. There is more to the business now, as they’ve added things like an advertising tier. When companies reach a certain size these sorts of numbers become less relevant, as was the case with AAPL 0.00%↑ which has a lot of revenue streams. I’m sure the Netflix subscriber numbers will also be slowing down a lot by 2025 when they’re set to axe the metric. They’ve squeezed all the juice out of this thing they can, the tailwinds from cracking down on password sharing have been realized.

"As we’ve evolved our pricing and plans from a single to multiple tiers with different price points depending on the country, each incremental paid membership has a very different business impact."

In 2023 they stopped providing quarterly paid membership guidance and starting in 2025 they will stop reporting quarterly membership numbers and ARM (average revenue per member) as this differs greatly by country, they have different tiers and now have more revenue streams like advertising.

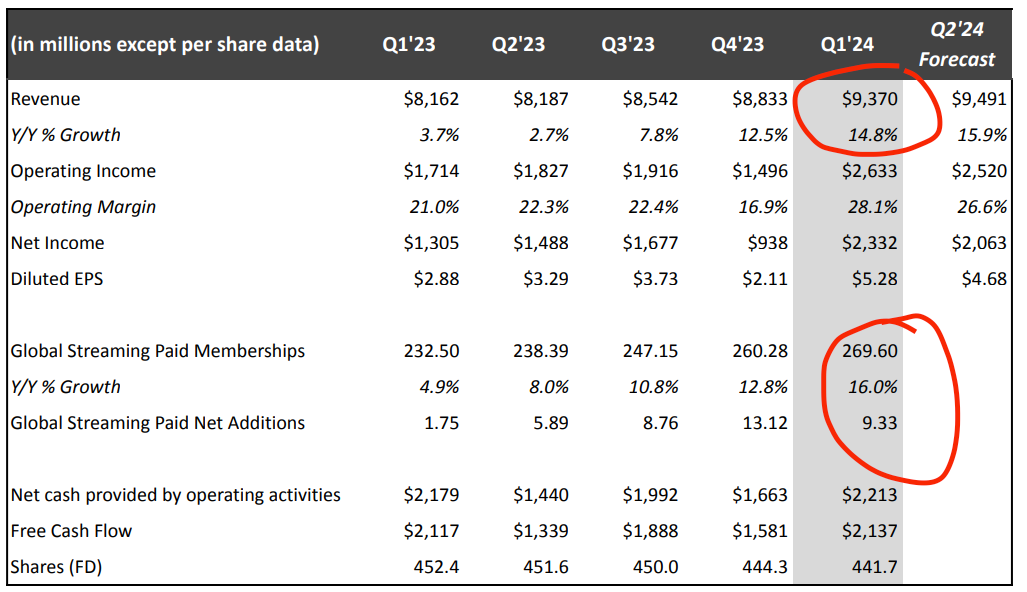

The company beat estimates and added over 9 million subscribers in Q1 while revenue grew 15%. They projected just under 16% growth for Q2 and the stock went down 10%. What more could Wall Street want? For the full year 2024 the company expects revenue growth between 13-15%.

Netflix is used in 270 million households, across more than 190 countries, with an audience of over half a billion people. No traditional entertainment company has ever reached this scale.

Their share of US TV viewing was up vs. recent quarters at 8.1%. There is still a lot of opportunity to capture from the slow death spiral of cable and traditional media, but outside that growth here will be hard to come by as the battle for peoples’ attention has become hyper competitive. At any given moment there are 100 things competing for our attention.

Netflix has taken up the strategy of broadening their offering which they’ve done well. In addition to appealing to different cultures around the world, they’re doing well adding specific niches to the offering. They will stream a live boxing match between Jake Paul and Mike Tyson this summer, an event sure to draw in boomers and Gen Z alike. They made an exclusive deal to broadcast WWE Raw which is sure to bring a unique and special group of viewers. This is in addition to a wide variety of entertainment that consistently sees top rankings, they had the number 1 streaming movie for 8 of the first 11 weeks of the year as well as the number 1 original series for 9 of the first 11 weeks. They continue to thread this needle nicely.

Financially things look great and Netflix continues to buy back shares, $2 billion worth in Q1.

On to the 2 problems I see long term. For starters, we have declining attention spans or as I like to call it, an attention span race to the bottom. Will millions of semi conscious Americans be able to sit through a 2 hour Netflix movie in 5 years? Or will they opt for 2 hours of mindless scrolling through 10 second Tik Tok videos. For the sake of us all I hope this trend does not continue.

On this note, the first problem is that the playing field has drastically changed from Netflix competing with traditional media to Netflix competing with everything like phones, social media and YouTube for attention.

A 2024 Spring survey found teens spend 29% of daily video consumption on Netflix, down 2% since Spring of last year, and 27% on YouTube, down 1% from last year. Competition is fierce and it is extremely difficult for Netflix to compete with YouTube, should that become the main competition, as YouTube brings in more revenue than Netflix with none of the production costs.

The 2nd problem is big tech players. Google and Meta, formerly Facebook, fit into both problem 1 and 2, but in the 2nd camp we also have Amazon and Apple. The threat from GOOGL 0.00%↑ and META 0.00%↑ is more short form, similar to Tik Tok and shrinking attention spans. But now you also have the bundling capabilities of companies like AMZN 0.00%↑ and AAPL 0.00%↑ to contend with. This bundling business model is a bit monopolistic and extremely difficult to compete with, but it remains legal for now. There are examples of pure players continuing to thrive despite it, Netflix and Spotify being great examples. Despite the entrance of Apple music, Amazon music, YouTube music and more, SPOT 0.00%↑ continues to grow and maintain its huge lead.

But companies like Amazon have deep pockets and major advantages. Prime video is just the cherry on top of an incredibly useful product in Amazon Prime. They’re getting better too, I just finished watching Fallout, it was great. Amazon could shower endless money into streaming if they wanted to, I would not want to compete with them.

Below is a chart on daily video consumption for teens from Fall 2023. As you can see, Netflix and YouTube are neck and neck, though YouTube has significant advantages on costs. There is definitely a lot of room for growth as traditional cable continues its decline.

Netflix has their work cut out for them, YouTube is a big threat and I outlined their major advantage. On this chart Amazon Prime and YouTube are the only ones I’d worry about for Netflix, there is opportunity to grow as the rest decline.

In conclusion, Netflix stock is currently around $555. If it were to tank more, I’d start to get interested around the $350 range. If it saw another 2022 type event where it got below $200, I would absolutely buy. Right now it will stay on my watch list. Join our community to see the stocks that I have been buying. Until next time!