Netflix Stock: The Streaming Wars Victor?

Netflix Stock: The Streaming Wars Victor?

A look at NFLX Q3

It’s Friday night. You’re about to watch the series finale of Breaking Bad and you’re hit with this message. This was my life last week. It was in that moment Netflix would convert a borrowing household into one of millions of new paid subscribers.

NFLX 0.00%↑ posted a great report as evidenced by the 15% jump this week.

I’ll go over the key takeaways and build on many points from my last Netflix article which you can read below.

The Results

Their outlook is excellent. Some concerns I mentioned in the last article were addressed: the company appears to be returning to a higher growth rate and is moving into some very intriguing new verticals including a real life Squid Game experience. They must’ve taken note of the 520 million views Mr. Beast’s $456,000 Squid Game In Real Life! video received.

Their password sharing crackdown is proving effective as evidenced by myself anecdotally along with 9 million new *paying* customers. Who would’ve thought that people who were not paying would start paying at a level greater than 0. Astonishing!

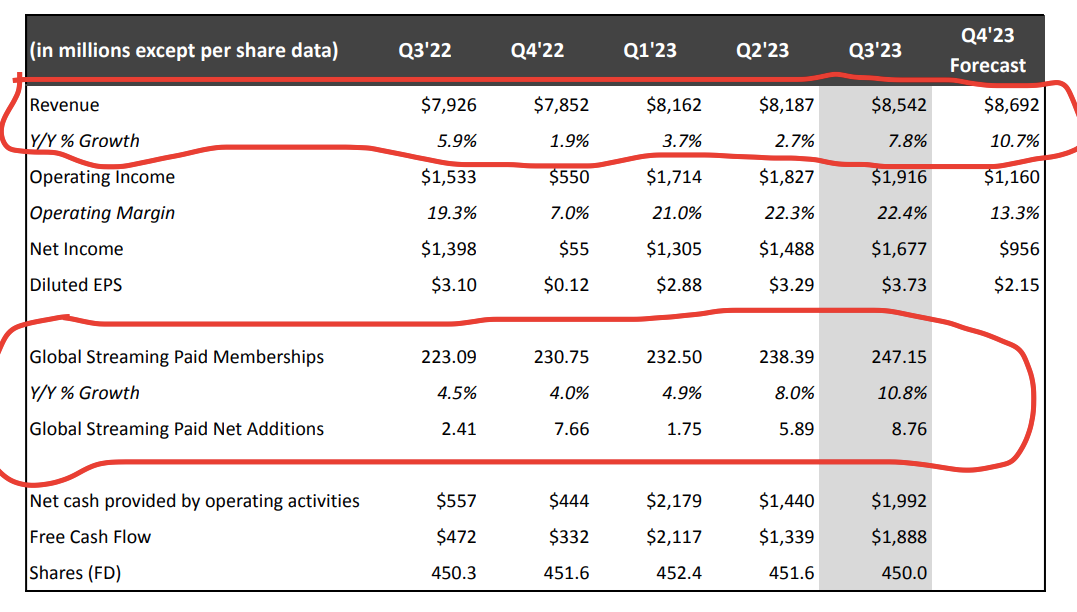

Revenue was $8.542 billion with global streaming paid memberships of 247 million, up 7.8% and 10.8% respectively.

As you can see above, growth rates are ticking back up to double digits after a tremendous slowdown, one of the concerns I previously highlighted in the last article. I maintain it’s an impressive feat to grow meaningfully in the current macro-environment.

Success in streaming starts with engagement. It’s our best proxy for customer satisfaction and when people are watching they are more likely to stick around (retention) and recommend Netflix to their friends (acquisition).

The variety and quality of our programming — combined with our reach (247M paying households globally and growing), superior recommendations and intense fandom — means we are able to generate higher engagement than our competitors.

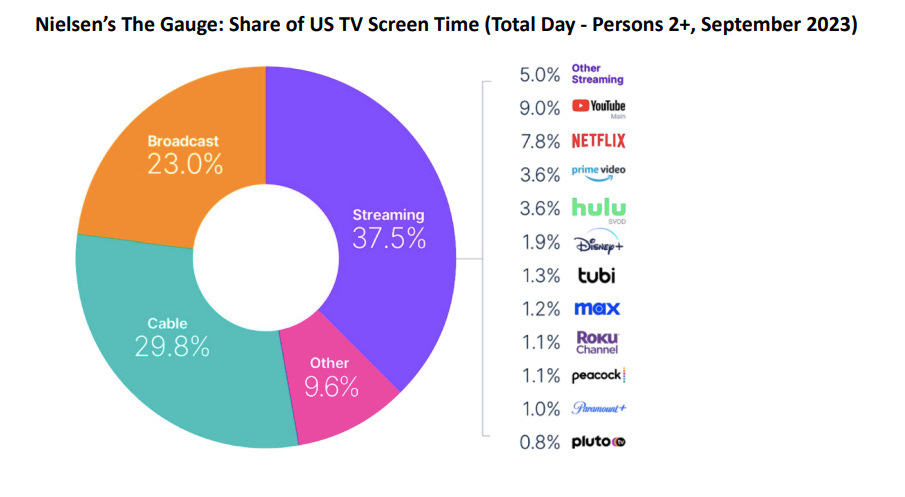

In the US, for example, we had the most watched original series for 37 out of the first 38 weeks of 2023 and the most watched movie in 31 of those 38 weeks according to Nielsen. - Netflix Q3

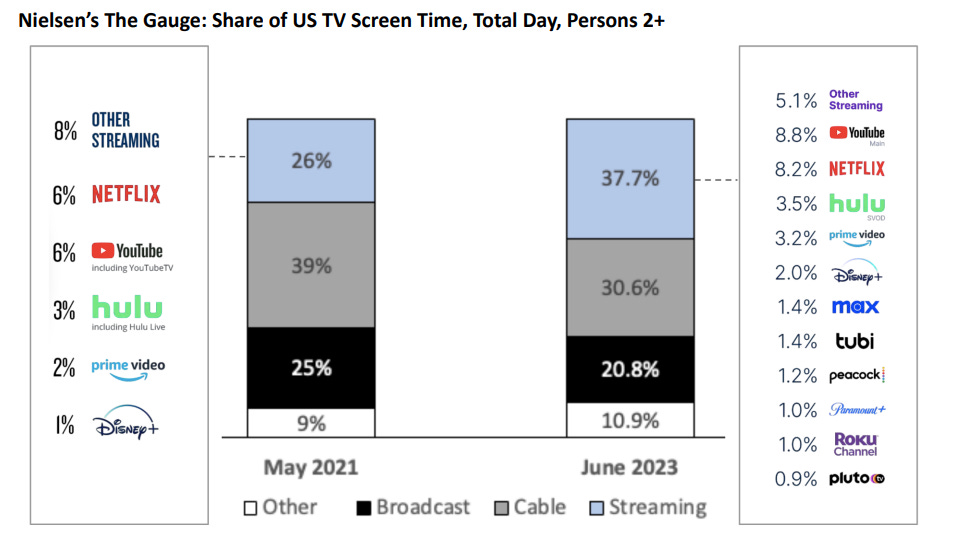

As you can see, Netflix is dominating the traditional streaming platforms. It is worth noting the risk of YouTube and changing consumer preferences. Below you will see the same chart from Q2. YouTube’s share has ticked up from 8.8% to 9% while Netflix is down from 8.2% to 7.8%. I’m not too hung up on this even though the company highlighted the importance of engagement, I focus more on the number of members.

Is there enough value offered to keep customers from cancelling their monthly Netflix subscription? I’m less concerned with whether people use the platform every single day or to what extent. Do I want to keep my Netflix subscription because there is at least 1 thing worth watching next month? That seems a better way to get the pulse of the business.

But, I suppose there are other benefits to engagement as they said above like recommending shows to friends which leads to acquiring more customers. Also, as Netflix moves more into an advertising model this does become more important, more on that later.

There is still 60%+ of dying market to capture made up of broadcast, cable etc. so as long as people still retain the attention span to watch something longer than 30 seconds, (God help us) then Netflix still has a huge runway for growth.

Where Netflix Shines

Netflix’s international approach seems to be having greater success than its peers. That’s because while the traditional companies have historically taken an outward-in approach exporting American content, Netflix has taken an inward-out approach, creating regional content that resonates in a specific country and ends up being popular internationally. Take Squid Game for example.

One Piece is a great example of Netflix’s variety, reach, recommendations and fandom at play. Based on the best-selling manga series, our live action adaptation generated stellar reviews, loud conversation on social media, in particular TikTok, and huge watching (62m views globally*) — making it our first ever 4 English language title to debut at #1 in Japan and pushing the series to #1 on Netflix’s global Top 10 for three weeks in a row - Netflix Q3

I used to watch this show as a kid. Netflix appears to be the only streamer pursuing this international strategy with great success:

Over 70% of our members are now outside the US… We are now producing or co-producing in over 50 countries and languages… In Q3, we saw big hits in every region and across multiple genres - Netflix Q3

What’s Next

We continue to innovate and invest in engagement off Netflix through our consumer products and experiences. Whether it’s Scoops Ahoy ice cream or Surfer Boy pizzas, our pop-up Netflix Bites restaurant or live Bridgerton Ball and upcoming Squid Game experience, fans of our shows and films want to engage more directly with these stories, including between seasons.

So over the next few years, we will be developing Netflix House — physical flagship destinations that combine fresh, new live experiences as well as food and retail so fans can visit many times a year safe in the knowledge there will always be something different for them to enjoy.

I said in the last article Netflix needed a new engine for growth, could this be it?

It’s early but this is definitely something to keep tabs on, watch out Disney World! DIS 0.00%↑

Netflix is moving into sports, they’ve had many viral documentaries and will have their first ever live sports event, The Netflix Cup on November 14.

Last but not least you have a huge opportunity in the advertising arena which is in early innings:

Adoption of our ads plan continues to grow — with ads plan membership up almost 70% quarter-over-quarter — and 30% of sign ups in our ads countries are, on average, to our ads plan, with more work to do to scale this business. Our $6.99 per month ads plan in the US continues to support our ads plan growth.

We remain very optimistic about our long run opportunity in this very big market ($180B ex-China and Russia). Ad dollars follow eyeballs and more and more TV viewing is shifting from linear to streaming — we’re a leader in streaming engagement, and the engagement of our ad tier members is strong. While we have much work to do to build out this business, we’re making good progress and laying the foundation for what we believe should be a multi-billion dollar revenue stream over time. - Netflix Q3

Conclusion

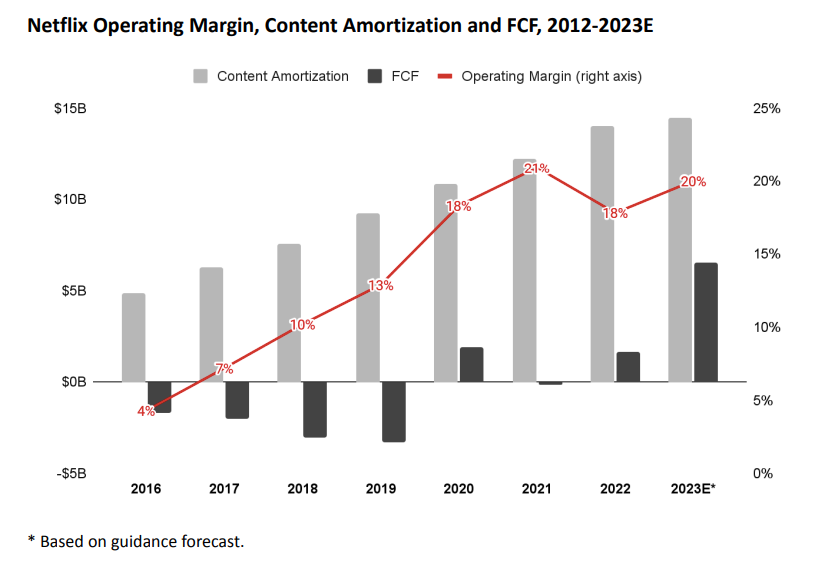

Free cash flow is on pace to increase significantly:

Things appear to be looking up for the company which saw its stock price decrease 70% in 2022. The balance sheet is strong, growth is accelerating and the company is buying back shares. Originally authorized to repurchase $5 billion, the board authorized an additional $10 billion for buy backs.

Netflix is on my watch list. While I don’t currently have a position, if I had to invest in a traditional streaming player (i.e. excluding Google/Youtube) it would absolutely be Netflix. I look forward to hearing what you think. Until next time!